The parties’ 2013 divorce stipulation of settlement provided that child support for their two children would be adjusted annually. Beginning May 1, 2014:

The parties’ 2013 divorce stipulation of settlement provided that child support for their two children would be adjusted annually. Beginning May 1, 2014:

“the parties shall set by April 30, a payment schedule of the Parent’s total obligation for base child support ‘made pursuant to the formula set forth below and income caps for the fiscal year beginning May 1 and continuing through April 30th of the following year. This schedule shall be based on the actual income’ for the previous calendar year. The Father shall then pay this base child support’ amount to the Mother in monthly installments.” [emphasis added]

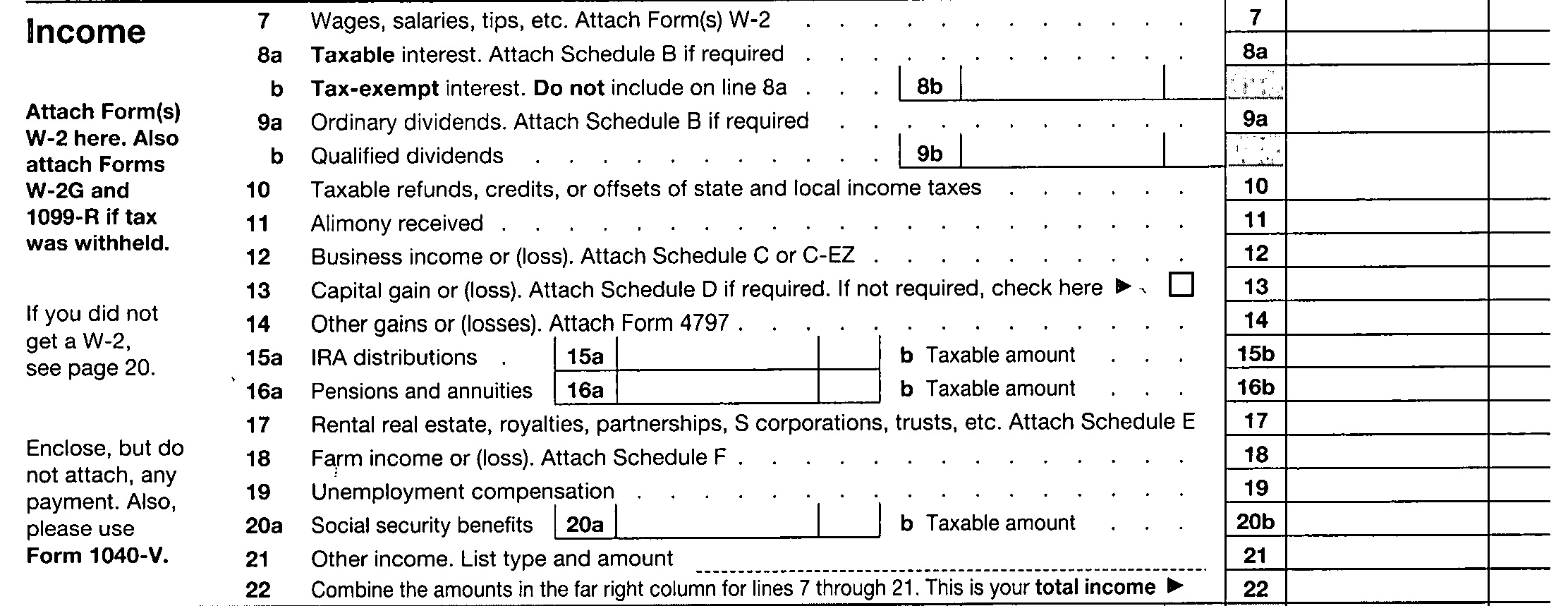

For the purpose of computing base child support, the stipulation defined “income” as “the gross earned income solely attributable to a party and as listed on the Form 1040 United States Individual Income Tax Return filed by the parties, less (1) FICA taxes actually paid; (2) Medicare taxes actually paid; less (3) New York City or Yonkers income or earnings taxes actually paid.”

In 2016, the mother received a salary of $86,801 for her work as a veterinarian. She also received $39,631 in “[o]rdinary dividends” and $245,629 in “[r]ental real estate, royalties, partnerships, S corporations, trusts, etc.” In 2017, the father calculated his base child support obligation using the mother’s adjusted gross income of $369,092. The mother disputed the calculation, contending that the income derived from her ownership interest in the LLCs was not “earned” income and therefore did not fall under the stipulation’s definition of “income.”Continue Reading Drafting Income Calculations in Divorce Settlement Agreements